6 West Hawaii Real Estate | August 3, 2018

MLS Statistics Real estate market doing well despite volcano

Iget asked daily how the market is

doing with all the news of dropping

hotel occupancy rates and Jack’s

Tours going out of business. So here

is my informal, antidotal story of what I

see happening in Kona. Saturday morning

for breakfast this weekend, the restaurant

on Alii Drive was busy, a friends oceanview

vacation rental in downtown doesn’t

have any more days available in 2018

since they have a full set of reservations

from now till the end of the year, and

well, Jack’s Tours is sad but their primary

business was bus tours of Volcanoes National

Park and the park has yet to reopen

after months of being closed. So, although

the hotel occupancy rate on the island has

dropped 6 percent, it is still in the high 70

percent range, which use to be very good

for us but with the recent upturn is a little

below the all-time recent highs in the 80s.

Real estate buyers are still buying.

We have 81 houses and 64 condos in

escrow as of this writing as well as 49

combined sales so far this month, just a

few days before the end of the month.

Now the sales number is arguably on the

low side but so were the house pendings

last month, so this may just be a delayed

swing from when no one knew when life

would return to normal in Kona, about

eight weeks after the volcano started by

my count. But it has returned to normal.

People are traveling here, people are

renting cars and buying houses, and we

are all so grateful that we are back on the

path to figuring out how to live with the

changes that the new eruption location

has brought into our lives.

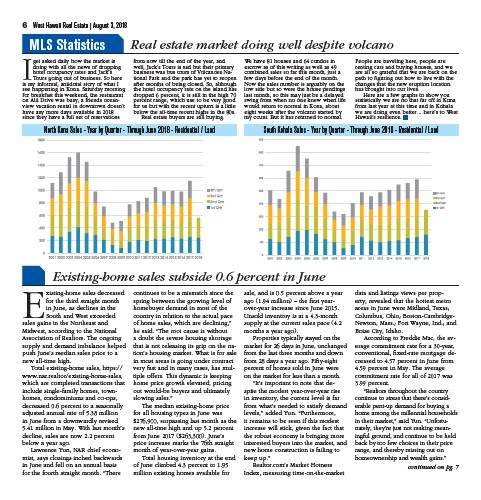

Here are a few graphs to show you

statistically we are no that far off in Kona

from last year at this time and in Kohala

we are doing even better… here’s to West

Hawaii’s resilience.

North Kona Sales - Year by Quarter - Through June 2018 - Residential / Land South Kohala Sales - Year by Quarter - Through June 2018 - Residential / Land

Existing-home sales decreased

for the third straight month

in June, as declines in the

South and West exceeded

sales gains in the Northeast and

Midwest, according to the National

Association of Realtors. The ongoing

supply and demand imbalance helped

push June’s median sales price to a

new all-time high.

Total existing-home sales, https://

www.nar.realtor/existing-home-sales,

which are completed transactions that

include single-family homes, townhomes,

condominiums and co-ops,

decreased 0.6 percent to a seasonally

adjusted annual rate of 5.38 million

in June from a downwardly revised

5.41 million in May. With last month’s

decline, sales are now 2.2 percent

below a year ago.

Lawrence Yun, NAR chief economist,

says closings inched backwards

in June and fell on an annual basis

for the fourth straight month. “There

continues to be a mismatch since the

spring between the growing level of

homebuyer demand in most of the

country in relation to the actual pace

of home sales, which are declining,”

he said. “The root cause is without

a doubt the severe housing shortage

that is not releasing its grip on the nation’s

housing market. What is for sale

in most areas is going under contract

very fast and in many cases, has multiple

offers. This dynamic is keeping

home price growth elevated, pricing

out would-be buyers and ultimately

slowing sales.”

The median existing-home price

for all housing types in June was

$276,900, surpassing last month as the

new all-time high and up 5.2 percent

from June 2017 ($263,300). June’s

price increase marks the 76th straight

month of year-over-year gains.

Total housing inventory at the end

of June climbed 4.3 percent to 1.95

million existing homes available for

sale, and is 0.5 percent above a year

ago (1.94 million) – the first yearover

year increase since June 2015.

Unsold inventory is at a 4.3-month

supply at the current sales pace (4.2

months a year ago).

Properties typically stayed on the

market for 26 days in June, unchanged

from the last three months and down

from 28 days a year ago. Fifty-eight

percent of homes sold in June were

on the market for less than a month.

“It’s important to note that despite

the modest year-over-year rise

in inventory, the current level is far

from what’s needed to satisfy demand

levels,” added Yun. “Furthermore,

it remains to be seen if this modest

increase will stick, given the fact that

the robust economy is bringing more

interested buyers into the market, and

new home construction is failing to

keep up.”

Realtor.com’s Market Hotness

Index, measuring time-on-the-market

data and listings views per property,

revealed that the hottest metro

areas in June were Midland, Texas;

Columbus, Ohio; Boston-Cambridge-

Newton, Mass.; Fort Wayne, Ind.; and

Boise City, Idaho.

According to Freddie Mac, the average

commitment rate for a 30-year,

conventional, fixed-rate mortgage decreased

to 4.57 percent in June from

4.59 percent in May. The average

commitment rate for all of 2017 was

3.99 percent.

“Realtors throughout the country

continue to stress that there’s considerable

pent-up demand for buying a

home among the millennial households

in their market,” said Yun. “Unfortunately,

they’re just not making meaningful

ground, and continue to be held

back by too few choices in their price

range, and thereby missing out on

homeownership and wealth gains.”

continued on pg. 7

Existing-home sales subside 0.6 percent in June

/existing-home-sales

/existing-home-sales